ONE: Results are in - Share price is up.

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 4,865,747 ONE shares at the time of publishing this article. The Company has been engaged by ONE to share our commentary on the progress of our Investment in ONE over time.

The results are in.

Sales up, revenues up.

Share price moving up...

Is an inflection point coming for our health technology Investment OneView Healthcare (ASX:ONE)?

Something is definitely up with ONE over the last two weeks:

The past performance is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

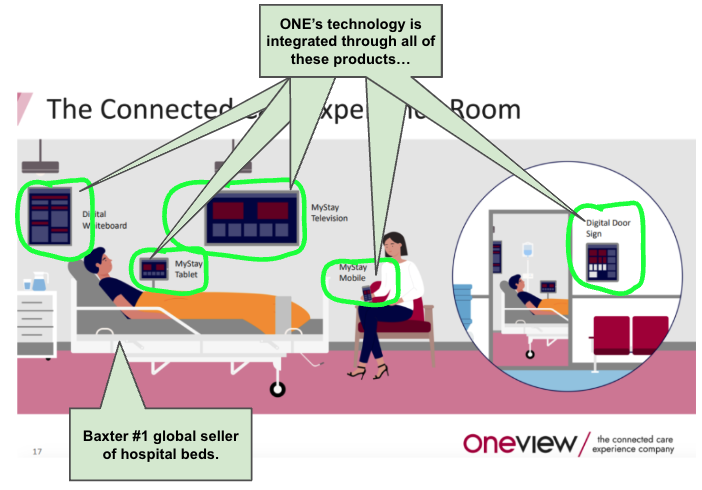

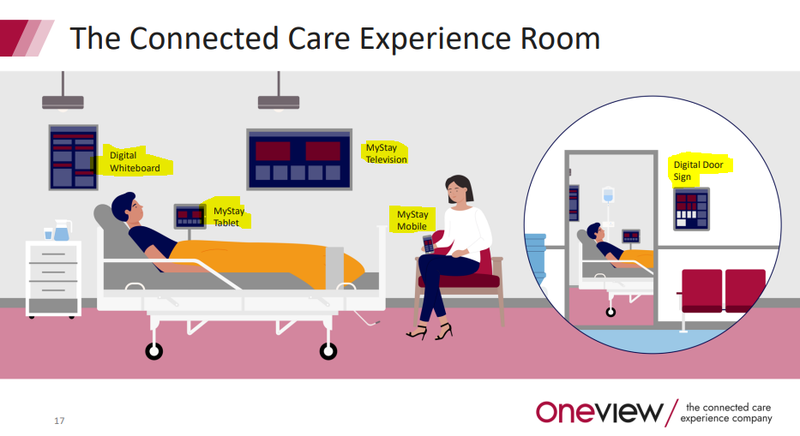

ONE sells technology to hospitals that improve the patient and nursing experience.

It connects the patient in the hospital bed to nurses, doctors, medical specialists, meal service, records, educational content, and entertainment.

ONE helps make hospitals run better and more efficiently.

(and for anyone that has been to or worked at a hospital, it can be incredibly inefficient at times)

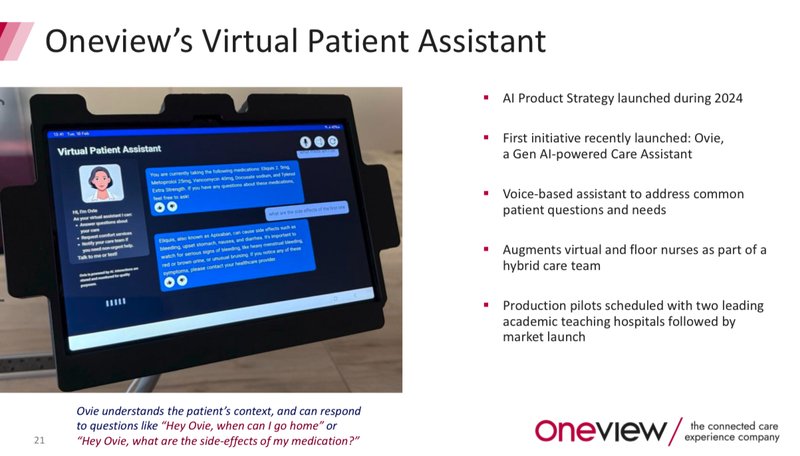

(ONE also just launched a new AI virtual assistant - further reducing pressure on nurses time by answering commonly asked patient questions.)

ONE just released its Preliminary final report for 2024.

Yesterday ONE hosted an “earnings call”.

An earnings call (a USA/Europe concept) is basically a conference call between a public company, analysts, investors, and the media to discuss the company's financial results.

...and provide an outlook on the year ahead.

(Also note that ONE’s financial year is the calendar year, so the FY ends at 31st Dec 2024)

Listen to the ONE call recording here

The accompanying ONE CY 24 financial results presentation deck is here

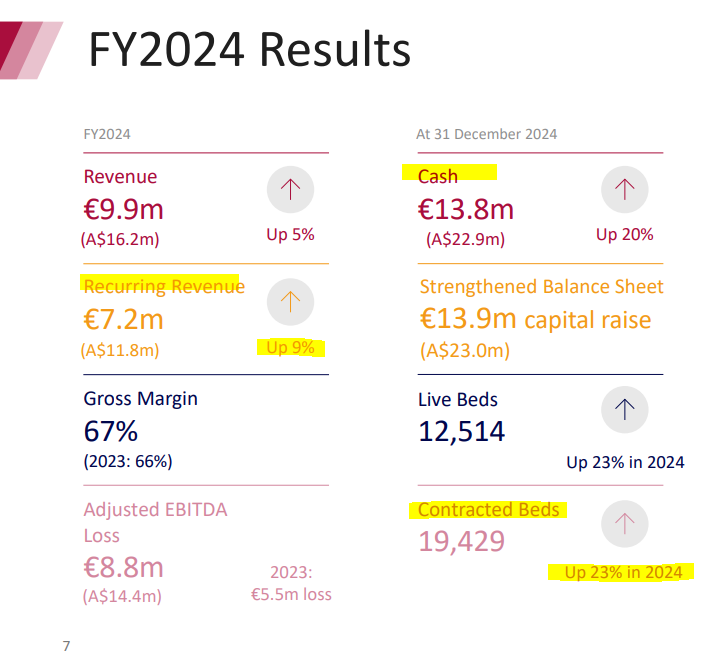

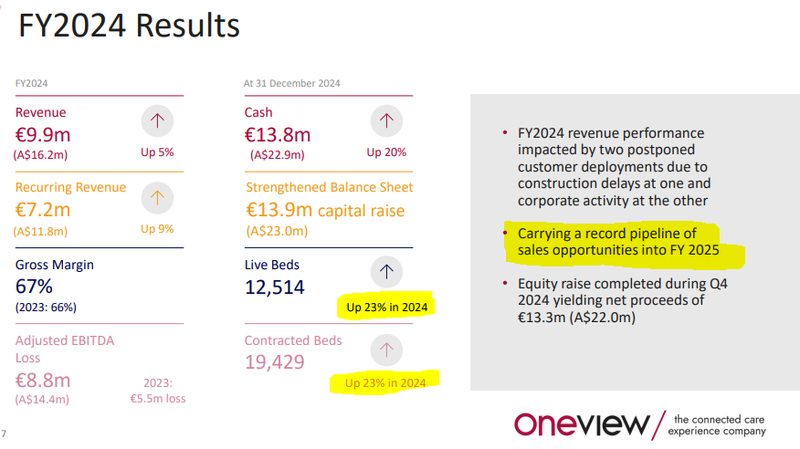

Some things we noted from the call and the presentation - ONE’s contracted beds and recurring revenue were both both up and ONE still has $23M cash in the bank (at 31 Dec 2024):

(Source - Slide 7)

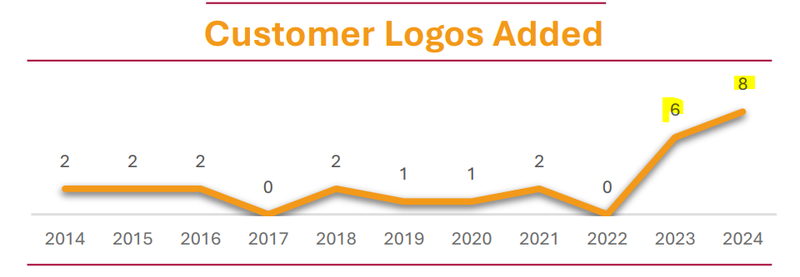

We also noted a record year for customer logos, with 8 new ones added in 2024:

(Source - Slide 11)

A “customer logo” in enterprise software sales means a new hospital has signed on with ONE, which usually starts as a small % of that hospital's total beds, that can be grown over time:

(Source - Slide 8)

Since we first Invested in ONE it has delivered strong progress and has moved up the ranks to in business maturity to gain coverage from analysts.

Most of ONE’s sales have been organic to date - meaning ONE has been selling direct to hospitals.

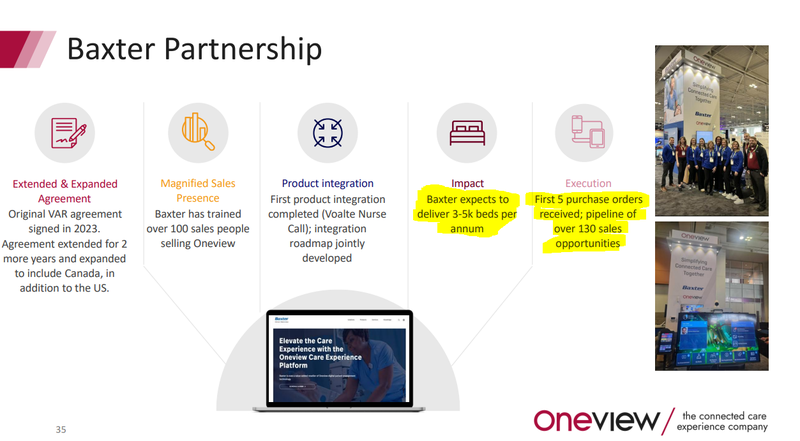

Then in 2023 it signed a sales partnership with the world’s biggest seller of hospital beds, $29BN Baxter International.

(the idea is that Baxter and its giant global sales team can get an edge in selling new beds to hospitals by bundling in ONE’s bedside technology, a win-win partnership)

According to the earnings call, ONE is going into 2025 with a “record pipeline of sales opportunities”.

Earlier this week ONE was roadshowing its product suite with its partner Baxter.

(Baxter is one of the world’s biggest hospital bed makers with ~75% market share in the US alone).

Hospital sales cycles are long, so Baxter sales should start kicking in very soon if the “record pipeline of sales opportunities” comment is anything to go by.

The “big two” in the hospital bed space...

Baxter is also seeing a push in its competitive landscape to adopt bed side tech - its big competitor Stryker (NYSE listed, $145BN market cap) has been going hard with M&A in the virtual care/bedside tech space.

Stryker and Baxter are the two biggest hospital bed makers in the world, locked in a Coke versus Pepsi, or Nike versus Adidas battle for hospital bed market dominance:

Stryker has been on an almighty acquisition spree making 54 acquisitions in the last decade or so, with an average deal value of US$743M. (Source)

Recently Stryker has been scooping up health technology companies left right and centre to improve its offering.

With Baxter meeting the challenge by adding complementary products and services as well.

Two interesting recent acquisitions by Stryker include:

- $3BN for a hospital staff communications platform called Vocera, and

- an undisclosed amount a few months ago for a company that does “AI-assisted virtual care workflows” called care.ai

If your biggest rival is going hard on bolt on technology deals to improve its hospital bed product offering, you need your own tech offering.

Especially for something like a hospital bed where sales are probably made on the margins...

and a nice bit of bedside technology could be the difference between beating your competitor to get a sale...

Baxter got the jump on Stryker by locking in a partnership with ONE back in 2023.

ONE’s partnership with Baxter...

This week Baxter posted some images co-branding its product offering with ONE at the VIVE2025 conference - a big event on the calendar for the digital health tech industry.

(Source)

Another thing we noticed was the buzz around AI at VIVE.

(Source)

Which is timely given the launch of ONE’s virtual AI product:

All this tells us is that bedside tech like ONE’s is becoming more and more important for the big players in the hospital bed space.

ONE has now finished developing its latest generation product suite - and is able to pitch its product as a complete hospital bedside technology solution.

(to complement channel partner Baxters hospital bed offering)

What we learned from ONE’s earnings call

We listened to the FY24 earnings call earlier in the week (unlike most Australian companies, ONE’s Financial Year ends at December 31st 2024), below is a list of some of our key takeaways.

Listen to the full earnings call here

Here are our key takeaways:

1. 6:09 - ONE signed 8 new logos in 2024 which is a record for the company in any single year. Across the 8 logos there are ~11,700 beds of which ONE has only contracted for ~33% of those beds for now. We think there is a good chance for ONE to slowly convert more of these beds into contracted beds.

2. 13:30 - CEO James Fitter talked about how hospitals were implementing virtual care systems into hospitals. There are many telehealth tech providers, ONE would be providing the “picks and shovels” (screens/tablets etc) for telehealth to be enabled in the hospital setting.

3. 15:40 - James talked about the virtual AI care assistant that was only launched a week or so ago. He also mentioned that ONE is now ready to market the product to potential customers. James also talked about how he was able to demo the product to some major potential customers and that the AI care assistant would be piloted across 2 hospital networks this year.

4. 23:00 - James talked about how over the past three years ONE has spent ~€29M on product development and has now become the most expensive/expansive product on the market. For us it means ONE would be hard to replicate.

5. 24:15 - James talked about how the US is the big focus for the company. He specifically mentioned that the real vision was to “work with our friends at Baxter to capture 15-20% of the US market”. He mentioned that there is ~900,000 hospital beds across the US, so 15-20% would be truly transformational for ONE.

6. 28:45 - James talked about the outlook from a product perspective. He specifically mentioned that the latest generation products (like the digital whiteboard, MyStay app and tablet) means that ONE’s sales pipeline is at record levels now.

Q&A Section:

7. 33:20 - MST’s analyst asked about the type of customers that the Baxter partnership is bringing in. James then answered saying it was a mix of sizes but was important because it would mean ONE could “land” and then “expand” in the hospital networks contracted. He also mentioned that most of the Baxter sales were for at least two of ONE’s products and in some cases three.

Key insights from ONE’s latest presentation

We also liked a few of the slides in ONE’s latest investor presentation.

Here are some of the slides that we thought were worth pointing out:

1. Live beds, Contracted beds & sales pipeline are all up

Live beds and the contracted beds numbers were already known from ONE’s December quarterly report.

But we did notice ONE mention that it was going into FY25 with a “record pipeline of sales opportunities”.

Given the partnership with $29BN Baxter International, we are hoping this translates to a step-change increase in sales this year.

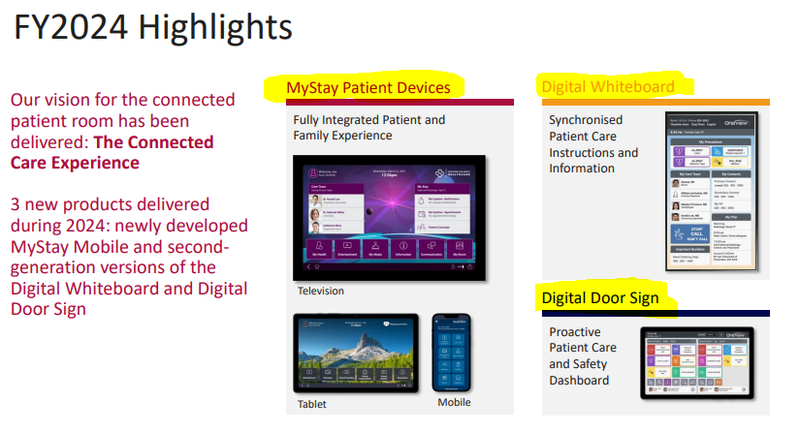

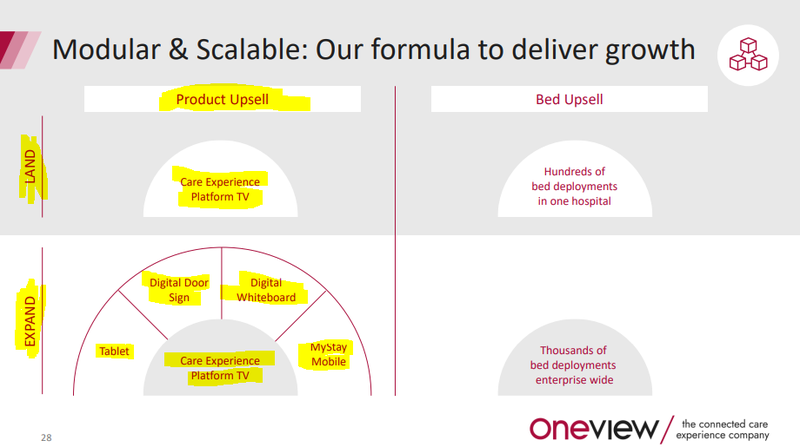

2. ONE delivered 3 key new products in 2024

The presentation also showed that ONE had delivered the latest generation for three key products - the MyStay BYO devices, Digital Whiteboard and Digital Doorsigns.

This may not seem like a big development because they were all previously announced products, but we think that by delivering an updated version of the product, ONE can now transition to focusing on selling the product as opposed to developing.

For us it's a signal that ONE is ready to market its full product suite as a one stop solution...

The slide from later in today’s presentation really hammered that point home:

3. We also noticed a big focus on “product upsell” opportunities.

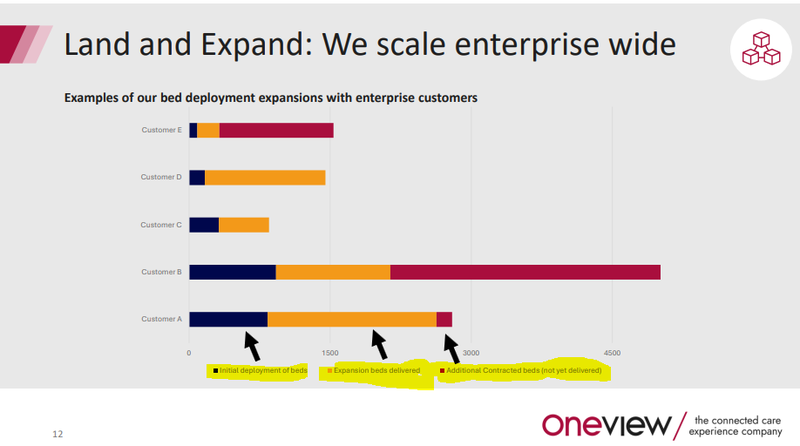

One recurring theme we noticed in ONE’s presentation was the idea of “land and expand” in the company’s value proposition.

(Here is our explainer on the “land and expand” strategy in enterprise software sales from 2021 - ONE goes for US market share ‘Land Grab’ with $20M Capital Raise)

This is a common sales strategy for enterprise SaaS companies.

Its basically getting your “foot in the door” with a small, quick and easy sale - then impressing the customer enough that they roll out the software across their entire organisation.

The slide on page 12 showed how that has worked for ONE in the past across 5 different customers.

So ONE’s land and expand strategy is working:

(blue is the smaller “land” deal, orange and red are “expand”)

We think ONE is approaching a point where the upsell potential for the company has increased significantly (especially with the key product launches mentioned earlier).

Now ONE can “land” a customer then sell more beds, and also upsell its Digital whiteboard, doorsign and Mystay offering.

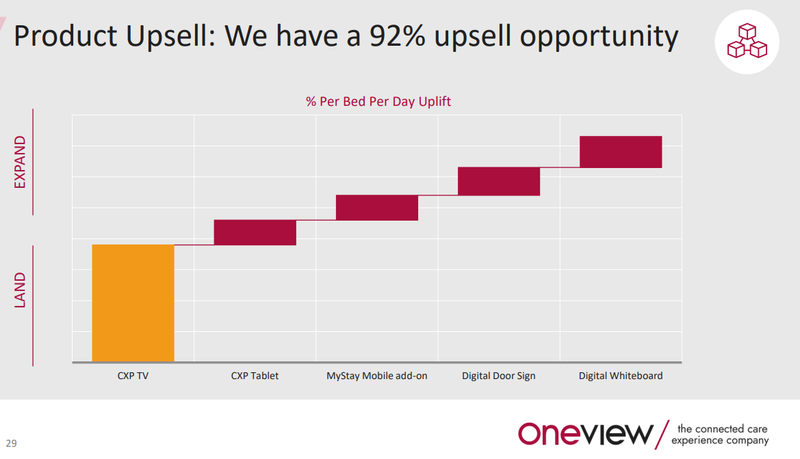

On page 29 of the presentation ONE mentioned there was a “92% upsell opportunity”.

We are hoping to see this strategy trigger a step change in sales for ONE in 2025.

The presentation overall is a pretty good run through of what ONE offers and what it is working toward.

Check out the full presentation here.

New analyst coverage for ONE published

We have seen three different analyst reports for ONE come out in recent weeks.

A common theme we saw in the reports was the recognition that ONE’s “land and expand” strategy was now starting to materialise into genuine sales.

The “land and expand” strategy is to win customers by providing the services to a fraction of the total beds under management and then expand through the hospital network off the back of doing a good job with the first few beds.

Basically let the product do the talking.

In the last two years ONE has signed up 14 new hospitals, and in the last year ONE has signed 8 new hospitals.

It is worthwhile reading these reports as they give a good overview of ONE’s progress through the lens of a financial analyst:

- MST Access Report with a price target of 49c.

- Bell Potter Report with a price target of 45c.

- Jeffries Report with a price target of 40c.

While these analyst price targets look pretty good, it’s worth noting that they are based on a number of assumptions that may not eventuate. Never invest on a price target alone, do your own due diligence before making an investment.

We think that 2024 was a very good year for ONE especially with the record number of new logos added.

We think that 2025 will be even better as it carries forward its momentum with new products and big brother Baxter on board.

Our ONE Big Bet:

ONE will sign on enough new hospital beds at an accelerating rate to achieve a $1Bn valuation (based on 5x to 10x forward ARR multiple) and be acquired by a large health tech provider.

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved, and it will require a significant amount of luck. There is no guarantee that it will ever come true. Some of these risks we list in our ONE Investment Memo.

What’s next for ONE?

Increase number of contracted beds 🔄

We are hoping to see more sales deals roll through and a conversion of sales through ONE’s value-added reseller partnership with Baxter International.

We especially want to see ONE hit 25,000 beds - it’s our number one objective for ONE in our ONE Investment Memo.

Update on Baxter deal 🔄

We want to see ONE start converting new sales from its pipeline with Baxter.

In the presentation from earlier this week, ONE mentioned 3-5k beds per annum from a current pipeline of over 130 sales opportunities.

What are the risks?

In the short term the key risk to our ONE Investment is “Sales risk”.

Sales Risk because there is no guarantee that ONE hits sales guidance that is in the market (and likely to be priced into the company’s valuation).

There is also a chance that the sales pipeline won't convert as quickly as we would like.

Large institutions like hospitals don’t tend to adopt new technology very often and the sales cycle can be long.

This feature of ONE’s customer base can cause delays in sales that drag out over a long time.

Our ONE Investment Memo

You can read our ONE Investment Memo in the link below. We use this memo to track the progress of all our Investments over time.

Our ONE Investment Memo covers:

- What does ONE do?

- The macro theme for ONE

- Our ONE Big Bet

- What we want to see ONE achieve

- Why we are Invested in ONE

- The key risks to our Investment Thesis

- Our Investment Plan

General Information Only

This material has been prepared by StocksDigital. StocksDigital is an authorised representative (CAR 000433913) of 62 Consulting Pty Limited (ABN 88 664 809 303) (AFSL 548573).

This material is general advice only and is not an offer for the purchase or sale of any financial product or service. The material is not intended to provide you with personal financial or tax advice and does not take into account your personal objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by 62C, StocksDigital, any of their related body corporates or any other person. To the maximum extent possible, 62C, StocksDigital, their related body corporates or any other person do not accept any liability for any statement in this material.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.